When studying economics in college, I assumed that investing and economics were sciences, where getting the right discount rate[1] allowed for the accurate valuation of anything. That turns out to be dramatically wrong. Instead, those seeking to become great investors would be better served in taking classes in evolutionary biology or psychology[2]. This allowance of human nature as the driving force of economic cycles can create great opportunities for those able to both recognize and capitalize[3] on it. I want to establish three points to get us started:

- Sentiment varies much more wildly than does reality

- The best investing is done when it is uncomfortable

- The most important question is “how much risk” is appropriate to take right now?

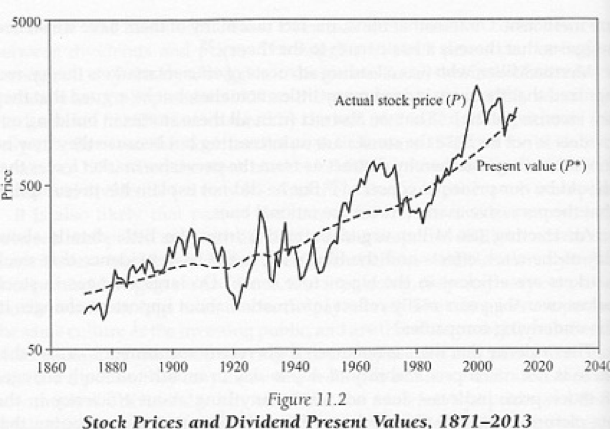

Sentiment varies more than reality. The image below is from Robert Schiller’s “Irrational Exuberance”. The dotted line is the present value of future dividends, which is where stock prices “should be” (what they were teaching us in school). The other line is the actual stock market. Dark line minus dotted line equals psychology. In real estate this can be shown via the fluctuation of property values much more wildly than the underlying Net Operating Income.

This discrepancy between sentiment and reality should create big opportunities for those who can buy when the dark line is below the dotted line and sell when it’s above! Sounds easy, but it’s not. It’s hard because it feels more comfortable to buy things that are going up. In reality, higher prices are riskier than low prices, but it doesn’t feel that way. For most “normal” goods (gas, burritos, TVs), when prices go down, people want to buy more. But for investing, our instinct is to the opposite. The trick is to overcome that instinct and to get aggressive when others are risk averse, and vice versa[4].

Thus, the best investing is done when it feels uncomfortable. Again, biology is not on our side, we we have evolved to steer clear of danger and seek safety. A good economy, with low rates, lots of capital and positive sentiment feels safe, thus we feel comfortable taking risks. Howard Marks – co-founder and Chairman of Oaktree – created the handy below table as a reminder that for investing, the worse things are, the better time it is to invest.

| – | + | |

| Economy | Vibrant | Sluggish |

| Lenders | Eager | Reticent |

| Capital Markets | Loose | Tight |

| Rates | Low | High |

| Spreads | Narrow | Wide |

| Owners | Happy to Hold | Rushing for Exits |

| Markets | Crowded | Starved |

| Funds | Hard to Access | Open to Anyone |

| New ones daily | Only the best | |

| Asset Prices | High | Low |

| Fund Returns | Low | High |

| Investors | Optimistic | Pessimistic |

| Sanguine | Distressed | |

| Eager | Uninterested | |

| Risk | High | Low |

| Mistakes | Buying too much | Buying too little |

| Paying too much | Walking away | |

| Taking too much risk | Taking too little risk |

It is easy to read this and say “Of course, buy when blood in the streets. Done”. But when the blood is actually in the streets it feels different. You start thinking “Wow, that is a lot of blood. I sure wouldn’t want that to be MY blood.” To get more objective, we can use data and metrics to help us establish whether we are leaning closer to the left (bad) or right (good) column.

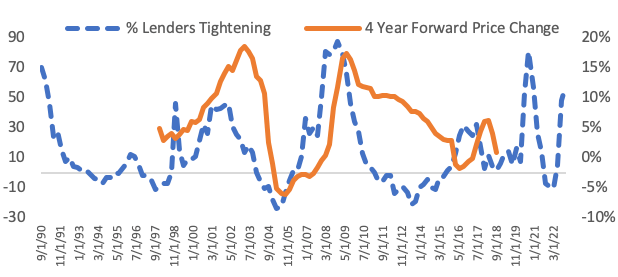

As one example, the graph below shows the proportion of lenders tightening their loan standards. This is compared to average annual change in real estate property values over the following four years. Periods of notable tightening ¾ such as the Dot-com bust and the Great Financial crisis¾ were the best periods in which to invest. The early 90s were a historically great time to acquire property as well, although the real estate data source doesn’t go back far enough. In the most recent reading, more than 50% of lenders were tightening, one of the highest readings in 30 years. Objective measures like this gives comfort that history repeats, and in previous periods, those taking more risks were rewarded.

All of this leads to the question of How Much Risk is appropriate today? We want to figure out where we are on the spectrum of those metrics and determine how much risk is priced into assets. We could attempt to put metrics on those categories on Mr. Marks’ table and determine a “Risk Score” and that is likely worth doing. However, a shortcut is to determine the amount of pessimism or optimism held by other market participants.

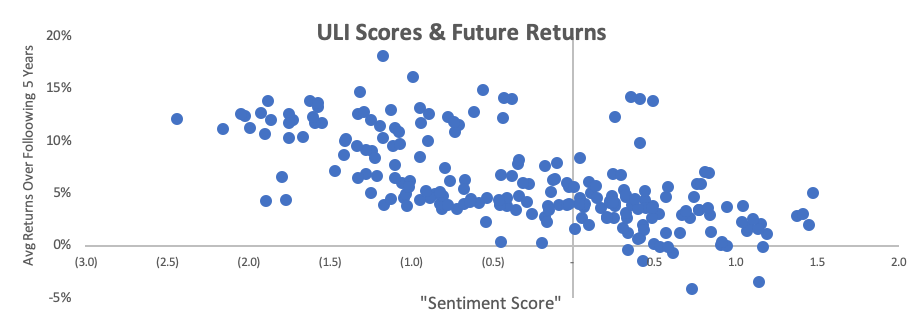

The Urban Land Institute releases an annual report called Emerging Trends in Real Estate in which respondents score all the individual markets by their perceived investment prospects. The graph below shows a normalized score for these responses, going back 20 years, compared to returns over the ensuing five years. The most “popular” markets in this survey have the highest “sentiment scores” and go on to have terrible returns over the following period, and vice versa. Popular markets have likely done well, and prices have gone up, and there are lots of buyers. High current prices equal low future returns, and vice versa. In the 2023 report, the least popular markets (after normalizing) were San Francisco and Portland. The most popular was Tampa.

The same exact building can be worth different values to different people, and different amounts to the same investor, at different times. There are times when an empty building is actually worth more than a full building and other times when that building worthless. These are mostly emotional distinctions, further influenced by other participants (investors, lenders, brokers, press, ratings agencies) who make up the market.

What can we say about the commercial real estate market today across our three key questions?

- Sentiment has become far more negative than is justified by the underlying economic reality, if measured by jobs and economic output. This is common, and at some point will overshoot in the other direction.

- It feels moderately uncomfortable to invest today, especially in out-of-favor sectors such as office where only the boldest are willing to tread. This discomfort should be interpreted as a positive signal for risk capital.

- The most sentiment indicators suggest considerable fear today, and Marks’ table shows that tightness in the capital markets and fundraising environments give clues for benefits to taking above average risk today. This suggests investors should take an above average amount of risk today given these factors.

[1] in our case studies, often to two decimal places

[2] I did take on Psychology class, but the most memorable part was the professor always started the class by playing the Peanuts song.

[3] Two different skills!

[4] As Warren Buffett said “the less prudence with which others conduct their affairs, the greater the prudence we should conduct our own”

Leave a comment